The UAE Corporate Tax return deadline is approaching fast — and for thousands of businesses with a December 2025 financial year-end, September 30, 2026 is the hard cutoff. Miss it, and automatic FTA penalties begin the very next day. Get it wrong, and you risk incorrect tax calculations, non-deductible expenses, and costly corrections. Whether you are an accountant managing your company’s filings or a business owner trying to understand your obligations, this step-by-step guide covers everything you need to file your UAE Corporate Tax return correctly, on time, and without costly errors.

Table of Contents

UAE Corporate Tax (CT) is a federal tax on the net profits of businesses operating in the UAE, introduced under Federal Decree-Law No. 47 of 2022 and effective for financial years beginning on or after June 1, 2023. It applies to business profits — not salaries, personal income, or dividends received by individuals.

The UAE CT regime operates on a self-assessment basis — meaning businesses are responsible for calculating their own tax liability, filing their own returns, and making payment without the FTA issuing an assessment first. This places the compliance burden squarely on the business and its finance team, making accurate record-keeping and a solid understanding of the CT Law essential.

For a deeper understanding of the accounting standards that underpin CT calculations, see our guide on IFRS vs GAAP — what UAE accountants must know.

Filing is mandatory for every Taxable Person — and this category is broader than many businesses realise:

A critical point many businesses miss: you must file even if your tax liability is zero. Non-filing triggers penalties regardless of whether any tax was owed.

The UAE CT return must be filed and any tax paid within 9 months from the end of your financial year. The FTA does not grant extensions — deadlines are fixed with no grace period.

| Financial Year End | CT Return Filing Deadline | Tax Payment Due |

|---|---|---|

| 31 December 2025 | 30 September 2026 | 30 September 2026 |

| 31 March 2026 | 31 December 2026 | 31 December 2026 |

| 30 June 2026 | 31 March 2027 | 31 March 2027 |

| 31 May 2026 | 28 February 2027 | 28 February 2027 |

Important: Both the return submission and the tax payment must be completed by the same deadline date. Filing without paying, or paying without filing, will both result in penalties.

Attempting to file without the right documents and data in place leads to errors, delays, and potential penalties. Before opening EmaraTax, ensure you have the following ready:

⚠ Key Requirement: IFRS-Compliant Accounts

The FTA requires financial statements prepared under IFRS (or IFRS for SMEs for eligible entities) as the mandatory starting point for all corporate tax calculations. Businesses maintaining accounts on a cash basis or in non-IFRS formats will need to restate their accounts before filing. This is one of the most common compliance gaps identified in UAE CT audits.

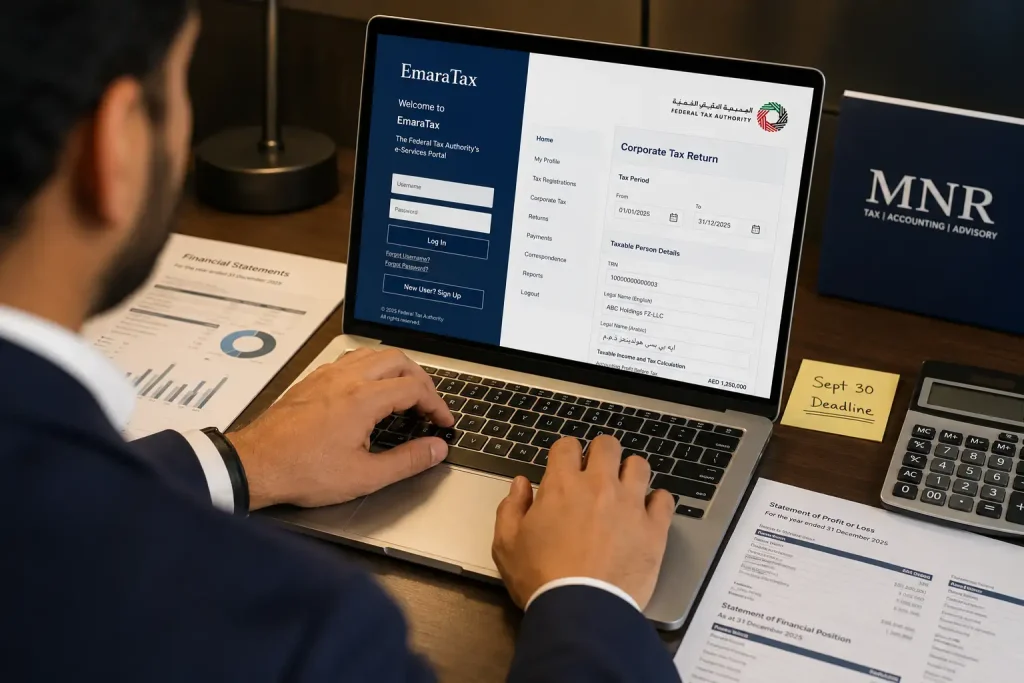

The entire UAE Corporate Tax return must be filed online through the EmaraTax portal at eservices.tax.gov.ae. There is no paper filing option. Here is the complete step-by-step process:

Go to eservices.tax.gov.ae and create an EmaraTax account if you do not already have one. Complete the Corporate Tax registration form, providing your trade licence details, Emirates ID or passport copies of owners, and company incorporation documents. Once approved, you receive your Corporate Tax TRN — you cannot proceed to file without it.

Log into your EmaraTax account. On the dashboard, select “Corporate Tax” from the left-hand menu, then navigate to “Returns” and select “File Return” for the relevant tax period.

The CT return form covers several sections you must complete accurately:

Review every section carefully before submitting. Once submitted, amendments require a formal request to the FTA and are subject to review. Make sure all figures reconcile to your financial statements before clicking submit.

After submission, proceed immediately to payment if tax is owed. Payment is made through EmaraTax via bank transfer, credit card, or approved payment channels. Both the return and payment must be completed by the same deadline date — late payment attracts its own separate penalty.

Taxable income does not equal accounting profit. The CT Law requires specific adjustments that every UAE business must apply before arriving at the figure on which tax is calculated.

The basic formula is:

| Item | Direction |

|---|---|

| Accounting profit (per IFRS financial statements) | Starting point |

| Exempt income (qualifying dividends, participation exemption gains) | Deduct (−) |

| Non-deductible expenses (entertainment excess, fines, personal costs) | Add back (+) |

| Interest deduction limitation (GILDR cap at 30% of EBITDA) | Add back excess (+) |

| Prior year tax losses (if carried forward) | Deduct (−) up to 75% of current taxable income |

| Free zone qualifying income adjustments | Deduct qualifying portion (−) |

| = Taxable Income | Apply CT rate |

Getting this calculation right requires a solid grasp of both accounting and UAE CT Law. This is exactly what Alifbyte’s Corporate Tax Training UAE course is designed to build — covering taxable income adjustments, exempt income rules, and GILDR calculations in practical, applied sessions.

The UAE applies a two-tier rate structure:

UAE resident businesses with annual revenue of AED 3 million or less can elect for Small Business Relief for tax periods ending on or before December 31, 2026. Under this relief, the business is treated as having zero taxable income — meaning zero tax liability — regardless of actual profits.

This is a transitional measure and expires on December 31, 2026. Businesses that qualify should strongly consider electing for this relief before the window closes, as normal CT rates will apply from the first tax period starting after that date. The election must be made when filing the CT return for the eligible period.

Free zone entities have specific rules that differ from mainland businesses, and many free zone companies have significantly misunderstood their obligations:

These are the errors that UAE businesses and their accountants most frequently make when filing Corporate Tax returns:

The FTA enforces UAE Corporate Tax compliance through a structured penalty regime. Understanding the penalties is a strong motivator for timely, accurate filing:

| Violation | Penalty |

|---|---|

| Failure to register for Corporate Tax | AED 10,000 |

| Late filing of CT return | AED 500/month (months 1–12) → AED 1,000/month thereafter |

| Late payment of tax due | 14% per annum on unpaid tax |

| Failure to maintain required records | AED 10,000 (first instance) → AED 20,000 (repeat) |

| Submitting incorrect information | AED 1,000 per instance (AED 10,000 if deliberate) |

| Tax evasion | 5x the evaded tax amount |

The best way to avoid these penalties is to understand the CT framework thoroughly before your filing deadline arrives. Alifbyte’s Corporate Tax Training UAE programme covers all compliance requirements, EmaraTax filing steps, and penalty avoidance strategies in structured, practical sessions delivered by qualified instructors.

For related compliance requirements, explore our guides on UAE VAT Training and UAE E-Invoicing requirements, which work alongside Corporate Tax obligations for most UAE businesses.

File Your UAE Corporate Tax Return With Confidence

Don’t navigate UAE Corporate Tax alone. Alifbyte’s Corporate Tax Training course equips accountants and business professionals with the practical skills to calculate taxable income correctly, file accurately on EmaraTax, and stay fully FTA-compliant.

→ Enrol in Corporate Tax Training UAE

Every Taxable Person in the UAE must file a Corporate Tax return — including mainland companies, free zone entities, foreign branches with a UAE nexus, and individuals whose annual business income exceeds AED 1 million. Filing is mandatory even if your tax liability is zero.

The deadline is 9 months from the end of your financial year. For businesses with a December 31, 2025 financial year-end, the filing deadline is September 30, 2026. The FTA does not grant extensions — missing this date triggers automatic penalties.

Register through the EmaraTax portal at eservices.tax.gov.ae. Create an account, complete the Corporate Tax registration form, and submit your trade licence, Emirates ID or passport copies, and company documents. You will receive a Tax Registration Number (TRN) once approved.

The standard rate is 9% on taxable income exceeding AED 375,000. Income up to AED 375,000 is taxed at 0%. Qualifying Free Zone Persons may be eligible for a 0% rate on qualifying income. Multinational groups subject to Pillar Two face a 15% minimum rate.

Small Business Relief allows UAE resident businesses with annual revenue of AED 3 million or less to elect for a 0% effective tax rate for tax periods ending on or before December 31, 2026. After this date, normal corporate tax rates apply. Businesses must still register and file a return to claim this relief.

Late filing triggers automatic FTA penalties of AED 500 per month for the first 12 months, rising to AED 1,000 per month thereafter. Late payment of tax due also attracts a 14% per annum penalty. The FTA does not grant extensions — deadlines are fixed.

Yes. All free zone entities must register and file annually, even if they qualify for the 0% rate as Qualifying Free Zone Persons. Filing is mandatory regardless of tax liability or exemption status.

UAE businesses must prepare financial statements under IFRS (International Financial Reporting Standards) or IFRS for SMEs. The taxable income calculation starts from the accounting profit shown in these IFRS-compliant statements, adjusted as required by the CT Law.

You can file yourself through the EmaraTax portal. However, given the complexity of taxable income adjustments, transfer pricing disclosures, and exempt income calculations, most mid-to-large businesses use a qualified accountant or registered Tax Agent. For straightforward SMEs claiming Small Business Relief, self-filing is manageable with proper training.

Alifbyte Educational Institute offers a comprehensive Corporate Tax Training UAE course covering registration, taxable income calculation, FTA compliance, EmaraTax filing, and post-filing obligations. Courses are available at Alifbyte’s Dubai (Al Karama) and Sharjah branches with flexible schedules for working professionals.